Chapter 3

Chapter - 03

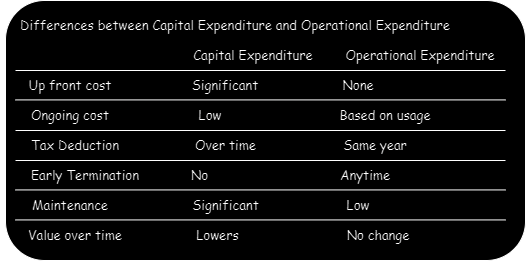

Differences Between Capital Expenditure (CapEx) and Operational Expenditure (OpEx)

Capital Expenditure (CapEx)

-

Definition: Capital Expenditure refers to the funds used by an organization to acquire, upgrade, and maintain physical assets such as buildings, technology, or equipment.

-

Nature of Investment: CapEx is typically a large, one-time investment that is aimed at creating or improving long-term assets. These assets usually have a useful life extending beyond the current financial year.

-

Impact on Financial Statements: CapEx is recorded on the balance sheet as an asset and is gradually depreciated over the asset's useful life.

-

Examples:

- Purchasing new machinery or equipment

- Constructing a new building

- Upgrading technology infrastructure

Operational Expenditure (OpEx)

-

Definition: Operational Expenditure refers to the funds that a company spends on the day-to-day operations required to run the business, including rent, utilities, and other operational costs.

-

Nature of Investment: OpEx is an ongoing, recurring expense that is necessary to maintain business operations and generate revenue. These expenses are incurred within the current financial year.

-

Impact on Financial Statements: OpEx is recorded on the income statement and is fully deducted as an expense in the same year it is incurred.

-

Examples:

- Paying employee salaries

- Utility bills (electricity, water)

- Leasing office space

- Software subscriptions or cloud services